Why Is This Housing Recession Going To Be Different for Bay Area Real Estate Market?

SHARE

Welcome to our August Bay Area Housing Market Updates. We have so much data to share as usual. You can find the video recording of this episode here.

Last month, we talked about six factors that can lead to a recession. There are two things that I want to go over again – GDP and the rising in unemployment.

Now, those are the two of the factors that typically we would consider part of the recession, aside from bankruptcy, defaults or foreclosures, high interest rates, falling asset prices, and lower consumer spending and consumer confidence. We’re going to touch on a little bit on consumer confidence as well today, but I really want to focus on these two, number one and number five, GDP and unemployment.

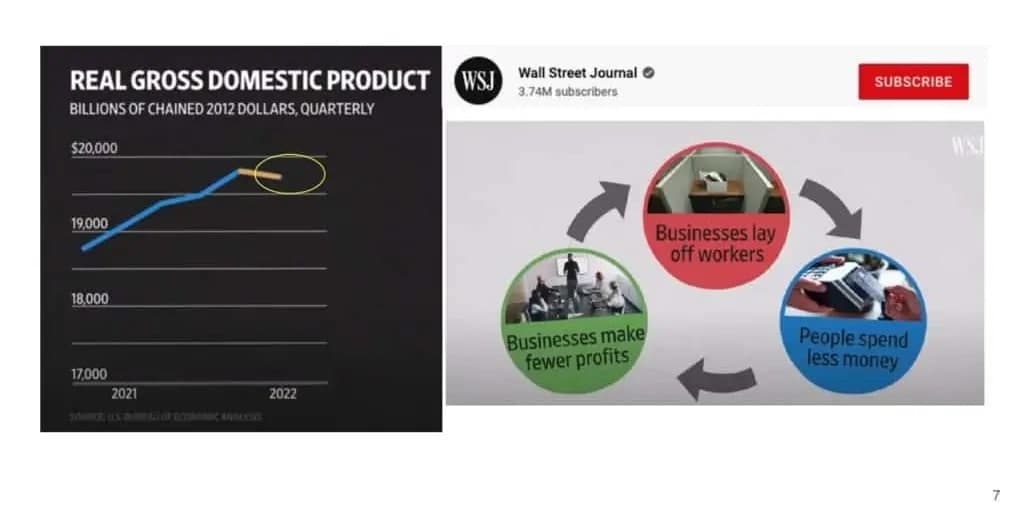

The reason why is that I just recently watched a video on youtube by Wall Street Journal and this is by John Helsenrath and he’s a Wall Street Journal senior writer. He said that this 2022 recession would be unlike any other. So, I was like okay I’m curious, I want to watch, I want to see what he means by that and the first thought was that he’s going to say this recession is going to be really bad and it’s going to be worse than the previous ones. And once I started watching it, I thought it was very interesting and that was kind of like what I’ve been talking about in our last episodes, why this recession is a little different and there are a lot of factors that we cannot really right away say that yes this is going to be really bad or it’s going to be okay.

One thing that we mentioned is the GDP. The way we consider there’s a recession is that we see there are two consecutive quarters of slowing down on the GDP which we do have right now. So, we are kind of considering that this is the beginning of the recession as one of the factors. The other one is that if the GDP comes down, then it can affect a lot of businesses and one of the three things that this video has talked about is that the businesses can lay off workers and also people spend less money and if people spend less money than these companies will make fewer profits and so this is like a cycle and then, of course, again the business will lay off workers.

With these factors, we also do know that with the businesses laying off workers, we’ve been talking about the unemployment rate being really strong these days and as a matter of fact we have this labor force participation rate that they show. Instead of people not being able to find work, it’s the other way around. The people are not really participating in the job market, and there are way more, record-high unfilled job rates instead since 2020. It just shot right up during this pandemic. As a matter of fact, we see everywhere that there is like hiring signs that companies are really trying to hire right now.

In a typical recession, for example, around 2001, the red line is the unemployment rate that’s going up as it should be, and then as the GDP comes down that should be the normal in past recessions. However, in today’s world, we are seeing the GDP coming down, but the unemployment rate is also coming down. I think that’s one thing really interesting and we had talked about it in the past episodes that the employment rate is still going strong. We are not seeing that it’s going up yet.

Then, on top of that, we look at the consumer confidence index. Now, we have a super, super high consumer confidence index in 2020, which went up to 41.4. We went from negative 33.4 bounced up to 41.4 as soon as the market kind of opened up. But now we see that it has come down to 1 in June of 2022. But, if we look at the chart at the bottom, we are seeing that we are right now slightly below the zero line and if we look back 25 years… I guess, we are still low but then we are not significantly lower than before and especially during the last two recessions. This could still continue to come down, don’t get me wrong, but it’s just that at this moment, the consumer confidence level doesn’t seem to be that low yet, although we do see a lot of pessimism in the market. I feel like it really depends on how the internet’s been sharing that information as well, but we definitely see that consumer confidence is getting lower.

Then in that case does that mean that this is actually making fewer profits? On the contrary, we actually see corporate have been having a really high profit margin and they also have tons of cash almost $4 trillion corporate cash on hand. So, businesses according to this youtube video with the Wall Street Journal, they’re saying that because the corporations have so much cash on hand and they’ve been making quite a bit of profit, it potentially could be that they have enough money, they’re not going to be laying off the workers because they still have enough money on hand and so if people have jobs still, they still have employment, then it may not actually really affect the economy or for example in our real estate industry, it is going to be affecting that much. But again I’m not here to tell everybody that oh, don’t worry about it our housing market is not going to crash. I just want to share with you the data that I found online and then also let you think about it. Think about whether this market is really going to crash or not and I definitely would love to hear what you thinking as well.

This is another article I read in Silicon Valley Business Journal. There are 3 big multifamily property sales in the Silicon Valley Market. Many of you know that I’m also specialized in multifamily and we always wonder, well, if the interest rate has gone up that means the cap rate will go up. If the cap rate goes up, will there be a lot of sales going on or will people be willing to sell or will people still be willing to buy because the rate continues to go up? And funny thing is that end of July, there are 3 investment firms, and different investment firms collectively spent nearly $575 million to buy three different apartment complexes in the South Bay. Now, the purchases are an indication that investors are bullish on the future of Silicon Valley’s economy. That’s one thing I thought about is that we have discussed before that there are a lot of companies, for example, Google; they’re building this massive, massive complex. In order for them to fill these complexes, they will have to continue to hire in the future, obviously not right now but in the future. They got to have some confidence in this market and then it looks like these investment firms; also have some confidence in this market. And they see that this optimism is that many of the region’s big tech companies expanded their office space during the pandemic and that’s the indication that they expect to continue to grow and higher and also many are requiring employees to be in the office at least few times a week and such mandates are going to ensure those workers will remain in the area and many will likely want to live near their offices.

We definitely have started to see a number of offices or a number of companies requiring their employees to come back to work at least part-time, 2 or 3 times a week. It will make it almost, at least to me, impossible to be living out of state and then come back 2 or 3 times a week just to work in the area. So we probably going to start seeing some people either moving over or coming back to the area in the future.

Now with that information, I want to share with you now with the Bay Area Housing Market Stats and see how it compares, maybe you are looking for a home right now, maybe you’re trying to sell or maybe you’re an agent trying to help your clients right now and so let’s take a look at the housing market stats.

First of all, we’re going to look at the offer Battleground. I call it a Battleground because it used to be really a battleground, you have to compete with 20 or 30 offers. Again, we now started seeing a lot of single digits. Surprisingly, there are still multiple offers unlike what the news might have said that the market is very, very cold. There aren’t a lot of buyers on the market, definitely have less but we still see multiple offers, right now, especially in the summer, typically it has already been slow every summer because families go on vacation. But right now, because of the inflation and because of the interest rate hikes, there are even less people coming out to look. However, they’re taking a pause doesn’t mean that they’re not looking. If the price is attractive enough, it will get them to come out and look at the properties and this is what happens is that we started seeing a lot of people put their very low offer price or asking price and attracted a lot of people to come in and then still have numerous multiple offers. The only difference is that now the multiple offers people are a lot more conservative when they are making their offers, they’re not going above and beyond the asking price.

Now, as an example San Leandro asking prices of $599,000; they sold at $765,000. It is still a pretty significant amount I think for this particular situation. In Fremont, 1.5 asking and sold for 1.6 with three offers. But then if we look at let’s say Santa Clara, the original asking for is 1.998 and it actually dropped to 1.95 and then now they received three offers and sold it, still sold it slightly below. That’s what we are seeing now, a lot of buyers waiting for the sellers to drop their price before they make an offer. This is another example, Cupertino, the original offer price was 3.886, they drop it to 3.595, they got three offers and then they sold it at 3.752. You can see the trend over here, it’s not crazy over asking price like before but we’re still seeing quite a bit of competition and we definitely seeing even more cash offers because right now a lot of people if they have the cash they definitely want to come out and use that as leverage to negotiate.

On top of that, we’ve been tracking the months of inventory. We’ve been saying that a normal market, equilibrium market is around 4 to 6 months of inventory and we used to be less than 1 month and that’s why you saw that everything comes on the market within the week, we sell it. And it started to climb up since May, June to 1.9 and then July went to 2.1 and it shot up all of a sudden in August to 3.8, close to 4 months now.

In terms of days on the market, we have gone from just a week up to almost 3 weeks, so I would say two and a half weeks around there. And then you see that people are definitely not as aggressive as before, they’re only offering right around the asking price and we started seeing a lot of people offering maybe slightly below asking price and if there are some multiple offers or they price it really low just to attract people, people are still not aggressively offering way above asking price.

In terms of the number of listings withdrawn or canceled, we’ve been seeing in Santa Clara County, San Mateo County, Alameda County and Contra Costa County, they all have been going up until June and then July actually they all started coming down a little bit on the withdrawn and canceled.

One of the main reasons I could see is that because sellers at the time when they’re getting their property ready around this time when they put it on the market that’s when it started to drop and at that point, they still wanted to be able to sell it at like the March valuation but they realized they can’t, so they were like okay we’re going to take it off the market and wait until the summer is over. By the time if they are putting on the market in the summer or July now, some of the sellers they really, really need to sell, they’re not going to take it off the market. This is also another reason why we’re continuing to encourage buyers in the summer, right now, August you still have some time, if you do see a property please do negotiate with the sellers because if the sellers are on the market right now typically they are really motivated and they really want to sell.

How many listing prices have been decreased? I was a little bit shocked, I know it’s going to continue to go up but as you see Santa Clara County, Alameda County, or actually real San Mateo County as well and Contra Costa County in the month of July, just jumped up significantly. I’m talking about almost three folds in July for Santa Clara County. That’s how many listings they have to drop their prices. I’ve heard so many people, some of the sellers and sometimes my friends of some sellers would tell me that they feel very discouraged, but I just want to again emphasize that this is the market unfortunately that we are in. It is really not your property per se but a lot of sellers are on the same boat and they all have to drop their prices during this time. And it’s almost like a strategy now because we mentioned earlier, a lot of buyers they wait for the list price to drop before they even make a move. So, work with your realtors®, and make sure that you are pricing your property the right way so that you can attract an offer.

But don’t worry! The sellers of the top 10 States that have the most dropping prices is not here yet, we see that in Boise Idaho 61% of the sellers are dropping asking prices; Denver, Colorado; Salt Lake City; Tacoma; Grand Rapids; Sacramento. Did you notice, these are all the areas that used to be the hottest market in the country, everybody wants to move to and now they’re also dropping prices as well. It is definitely happening all over the country.

In terms of Transactions Fell Through, I feel like the numbers even though it is increasing is not as much as I thought because one of the things is that some people think well if the market is changing, some buyers may have gone under contract and then they regret it. It’s like, Oh, my God, the market is dropping so I better pull out. I would much rather to lose my earnest money deposit than going in. Although, we are definitely seeing more but considering four counties combined, we’re only seeing less than 200 deals that have transactions fell through. It is not as bad as I thought it would have been considering how much internet news about how bad this housing market is going to go.

Now, in terms of the Median Sales Price, it is definitely coming down for these single family homes prices. In Santa Clara County, we had gone down to $1.65 million from the highest at 1.95 and then San Mateo county, it went from the highs at 2.25 in April came down to $1.8 million and Alameda County went from 1.5 in May now came down to 1.225 and Contra Costa went from the highs at 980 now came down to $860,000. They kind of came down about 20% from the peak in 2020. But if we’re looking in terms of like from last month we came down about 4% for Santa Clara County but actually it’s still positive from last year of August and in San Mateo County, it didn’t change from July but from last year, it came down to 2.7%, Alameda County came down 4.67% from last year and Contra Costa County, came down 1% from last year.

So, the biggest question is, is the housing market going to crash or not over here, right? And there’s this big debate, I guess they’re not really debating, it was just Dave Ramsey who’s very vocal about that he doesn’t think there’s going to be a housing market crash. One party thinks that there’s going to be a surge of inventory coming onto the market because all the sellers who did not want to sell yet think that the market’s going to continue to go up and then now they’re going to start coming back out to sell their property. Dave Ramsey is saying that look our current supply is just not high enough.

Compared to 2007, we have 3.7 million properties on the market, right now we are only one-fourth of what we used to have. So, there’s no way we can even catch up to the 2007 level. There are these two debates.

So that’s why I’m curious. I just wanted to look at the supply in our counties versus our demand. If we look at the supply definitely has gone up, if we just look at the past 12 months is at 9774 listings, this is active listings and if we’re looking at the differences between the supply and sold, what we see is that mostly there are about 2000 something listings differences and including this one is probably one of the largest differentiation would be about 2000 something listings differences.

Now, we have this one in 2021, we actually have a little bit more sales than the active listings coming on the market. But, if we look at July, this differentiation we have about 5727 is probably one of the largest. What I’m trying to show here is that we do have a higher supply compared to the last 12 months and we do have a quite low of demand compared to the last 12 months.

But if we go back 3 years and look at 3 years’ number then we see that our supply here is actually not the highest. We are kind of still lower than the 2020 level and also definitely lower than the 2019 level demand in terms of like how much sales we had, it is one of the lower ones. We are lower than 2019. I mentioned 2019 is because we also had a slowdown in the market at the time the property stayed on the market a little bit longer as well.

By looking at the differences between the active listings and the number of sold we can see that this is actually not as much as the 2019 level yet, so the demand is not as high as before but then the supply is definitely not as high as in 2019 and then the difference is actually smaller than 2019.

What can affect the demand on the market? So, we’re going to look at one of the biggest factors right now is because of the interest rate. As always we track Freddie Mac, Fannie Mae, Mortgage Bankers Association, and National Association Realtors®, their projections and they have been increasing their projections on their mortgage rates. We definitely see that they are going up but this seems like the 4Q, they’re all topping at 4Q and then for Freddie Mac, Fannie Mae, and Mortgage Bankers Association expecting they’re starting to stable and slowing down or maybe come down slightly 2Q 2023 and 3Q 2023. So that can absolutely affect your demand.

Also, CNBC had a segment and then they looked at the Consumer Housing Intentions by UBS Lab Survey, and 36% of people that they surveyed plan to purchase a residential property in the next 12 months. We mentioned again a lot before that a lot of people are taking a pause to buy, they’re not stopping buying properties, they’re just planning to purchase that later in the next 12 months, they’re observing right now. And then there are 27% plan to sell their home in the next 12 months and 66% believe that finding an affordable home will be somewhat too very easy in the next 12 months. Definitely, we’re going to see some increase in the demand to purchase property again and I think that the price will drop to a level where people are going to just come back out and say, you know what, even with a high interest rate I think it is time to come back out to look because at the end of the day we want to know whether the supply is really satisfying the demand that we have.

Now, speaking of supply, of course, we really, really need to rely on construction in order to satisfy the supply and we’ve been talking so much about the shortage of housing in the country and especially in California.

Helen: In California, we’re short about 2 million units, is that number about right?

Greg Paquin: I think it’s a bit exaggerated but there clearly is demand in California for housing.

Helen: How many units do you think are really short by?

Greg Paquin: I think we overestimate the number of units that are in demand based on, not only population growth but household formation and we’re seeing an exodus of people right now and I have a slide that shows that in the Bay Area but as a state as a whole more people are leaving than are coming. So, the population is actually declining. And part of that is that housing is just so unaffordable, it takes a long time to get housing built and certainly higher interest rates aren’t helping that at all, right now. I think that number tends to be exaggerated, I also think that you know the aging of the population is quite a significant baby boom population in the State of California and those folks are going to be making decisions. Not only will they just be dying because they’re getting older but they may be moving into other facilities whether it’s active adults or assisted living type, memory care things. And there’s going to be a transfer of those units to younger folks so that may alleviate some of that demand for newer construction than we would project. I just think that the governor had come out 2 years ago, I haven’t heard much about it lately but he came out earlier and said that we need, I forget the exact number, x number of millions of houses built per year and I think that number was exaggerated.

Helen: So exaggerated, we would say about half of it would be more likely the number.

Greg Paquin: I think so. Yeah, I mean it’s probably reasonable. Again, I don’t recall the number but we’re just not seeing population growth as significant as it was 20 years ago or 30 years ago.

Helen: That’s good to hear in a sense that we are at least not as bad as we thought but at the same time I’m really curious to hear about whether the construction is really continuing to increase or not and then like this chart or this graph has shown by CNBC is saying that actually housing completion we’ve done better than last year. We had increased 9.3 percent of the housing construction. That’s great news because we definitely need more supply.

Jerry Howard is the CEO of the National Association of Home Builders. He does feel that the market is definitely suffering. He says US homebuilders’ sentiment falls. I think this is a good time to hear from our guest speaker Greg Paquin, because he gives a lot of these home builders his advice. Watch the full episode of August Bay Area Housing Market Townhall – Current and Future Trends of New Homes Market on our YouTube Channel!

I hope that our audience got a lot of great information from this month’s Bay Area market updates. The most important thing is that we are sharing statistics with you just so that you can make the right decision for your own investments, or if you are an agent, use that information to advise your clients. So hopefully, I will see you next month, register here to join us live every third Wednesday of the month!